Basel IV is widely framed as a banking regulation story. It is. But the implications for corporate borrowers are receiving almost no attention outside of bank risk committees and that asymmetry is worth naming.

With Basel IV already live in the EU, finalized in the UK and under active proposal in the US, banks across major markets are reassessing the balance sheet efficiency of certain lending categories. Capital requirements are increasing. That makes certain loan types more expensive for banks to hold. The adjustment will not arrive as a sudden policy shift. It will show up gradually in renewal conversations, covenant adjustments, and in pricing that moves just enough to be accepted rather than challenged.

The companies with the most exposure are mid-market borrowers in sectors banks have historically viewed as difficult to underwrite: businesses running complex cross-border supply chains.

It Is Not Just a Mid-Market Problem

The pressure on investment grade corporates will be subtler but no less real. For larger borrowers the issue is less about access and more about terms, flexibility and the durability of relationships that have historically felt secure.

Basel IV makes visible something that has always been true but easy to defer: a debt capital structure that cannot adapt quickly is a liability. The ability to move between programs, adjust funding mix and maintain leverage with banking partners is becoming a strategic capability, not just a treasury preference.

Alternative Capital as a Strategic Advantage

The capital rules driving this shift apply to banks. They do not apply to non-bank lenders, and that distinction matters structurally. Institutional capital has been moving steadily into alterative capital structures for several years, and the private credit market is projected to nearly double in the years ahead. Alternative capital providers are not filling a gap out of opportunism. They are operating under a genuinely different set of constraints.

For mid-market companies and structurally more complex borrowers, building alternative capital funding relationships before a renewal cycle comes under pressure is the more resilient strategy. That requires more than identifying alternative lenders. It requires the systems, data and infrastructure to manage programs across multiple funding sources and maintain visibility across structures when conditions change.

Technology is Where the Operational Advantage Lives

Basel IV limits what a bank can hold on balance sheet regardless of how sophisticated its credit models are. But the constraints here are structural and that’s exactly where the opportunity lies.

Alternative capital platforms can deploy technology as a genuine operational advantage rather than a tool for managing regulatory overhead. And for borrowers, the more meaningful opportunity is upstream: real-time working capital visibility that gives CFOs the ability to see structural changes in their funding picture early enough to act, rather than discovering a facility will not be renewed when alternatives are already limited.

The Conversations Are Already Starting

The adjustment banks are making is already underway – partnering with alternative capital providers to manage working capital at the portfolio-level. Some corporate borrowers will find themselves navigating a shorter runway than they realize, particularly those approaching facility renewals in the next 12 to 18 months without a clear view of alternatives.

The most important question for any treasurer right now is not whether their current facilities are performing. It is whether their funding structure is resilient enough to absorb a shift in their primary lender’s appetite without disruption.

As capital markets continue to evolve, the companies best positioned for resilience will be those with the visibility, optionality and Connected Capital infrastructure needed to adapt with confidence.

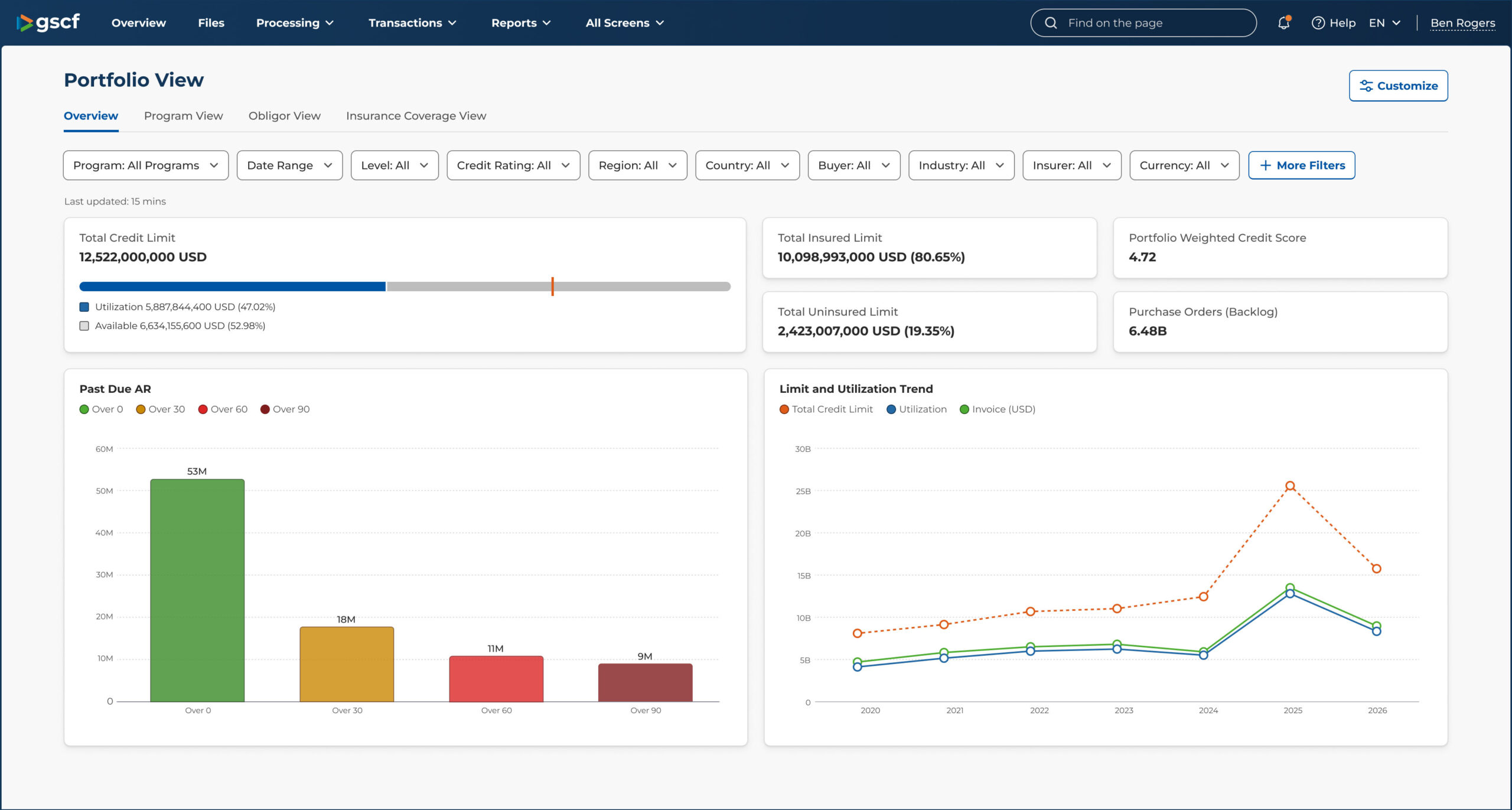

Learn more about C4: Connected Capital Control Center, GSCF’s platform for working capital at scale, delivering portfolio-level intelligence, real-time decisioning and unified control across every working capital program.